Beyond Meat : the lowdown on the alternative proteins champion

By David Stevenson on Saturday 10 July 2021

By David Stevenson on Saturday 10 July 2021

Future Food Finance take an in-depth look at Beyond Meat, delving into its financials, business model and share price performance as well as scrutinising recent trading of the California-based plant-based meat-maker.

Beyond Meat is arguably the poster child for the imminent alternative proteins foodtech revolution. It boasts a well-known brand name in a market that even sceptics think will reach $8 billion (£3.45bn) in just four years.

Crucially, Beyond Meat was also the first really big player in this space to list on the public markets back in May 2019 when its shares debuted at $65 (£45.90) before then racing up to a peak of $234 (£165) in July of that year.

Since then, Beyond Meat ’s share price has yo-yoed around as the first chart below shows.

In this article we’re going to dig a bit deeper into its reported numbers to establish whether that price volatility is warranted. We’ll also try and put some sensible metrics on those valuations – marketing hype about a coming revolution in food is all good and well but, at some point, the hard numbers need to prove current valuations.

That has been made especially difficult as recently Beyond Meat became yet another candidate for the Reddit brigade, especially after Jim Cramer, the former hedge fund manager turned TV personalteiy, talked about the stock on his CNBC program Mad Money recently, arguing that its sales might grow dramatically after the lockdown.

This must have come as a great relief to Beyond Meat as in recent months its shares have also been the subject of fairly pronounced short activity.

in late January, for instance, its shares were up in a short selling squeeze with nearly half of its stock shorted at the time.

It’s worth noting that as of mid May that short interest was still very high at 14m shares outstanding and a days to cover ratio of 3.38 according to Nasdaq.

Beyond Meat share price since IPO

Blue line represents S&P in same period

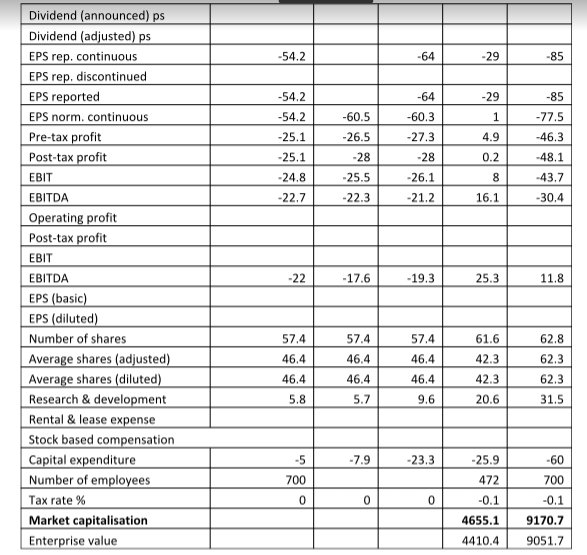

In it’s most recent quarterly results, Beyond Meat announced that it lost $25.1 million (£17.65m), or 40 cents (30p) per share.

According to a Barron’s report on the business at the time, it said "on an adjusted basis, which excludes expenses related to the Covid-19 pandemic, it lost 34 cents (26p) per share. Revenue rose 3.5 per cent to $101.9 million (£71.95m). Analysts were looking for a 14 cent (11p) per-share loss and revenue of $103.6 million (£73.16m).

“The company said that the Covid crisis continues to weigh on its food service channel because fewer people are dining at restaurants. Revenue at that segment was down 42.6 per cent.

“In addition, a surge in supermarket sales the company enjoyed earlier in the pandemic, as consumers stocked up on groceries, has 'moderated,' it said. Still, retail sales were up 76.3 per cent from a year earlier. Citing uncertainty related to the pandemic, the company declined to provide a full-year forecast.”

Not unsurprisingly these results were not greeted with much enthusiasm by the markets but we would argue that it is probably not fair to read too much into these numbers – many analysts think, like Cramer, that the business is now set to grow exponentially again post pandemic.

The key for Beyond Meat is that it sells mostly – to date – down a wholesale route via key commercial partners to whom it supplies its plant-based meat alternative. And on this front it’s clear that Beyond Meat has been building an impressive list of partners, especially on the foodservice front.

These relationships include:

This enviable roster of food service partners also opens its up to an obvious risk – during lockdown customers have mostly avoided indoor dining in favour of drive through and takeouts.

That’s led some analysts to worry that with outfits like McDonalds focusing on cutting service times to the absolute minimum, its partners will end up narrowing down their product range – and leave off plant based alternatives as a choice. Menu streamlining could, thus, work against Beyond Meat .

Analysts have also pointed out that Beyond Meat is also behind the curve when it comes to increasing demand – especially in Asia – for white meat alternatives.

Chicken sandwiches are proving hugely popular in McDonalds and Wendy’s and although Beyond Meat is working on a product it’s not in any restaurant at the moment.

Moving away from foodservice partners, Beyond Meat is also ramping up its product distribution into supermarkets especially into Europe where it has just opened a huge new factory in the Netherlands. Beyond Meat is telling investors that it expects solid second quarter growth and we see no reason why we shouldn’t see surprises on the upside in terms of sales growth.

But we also need to be aware that Beyond Meat is in an increasingly competitive environment. This competitive landscape revolves around three key dimensions. The first is price. Alternative proteins are still priced as a premium product compared to meat and the push is to get the griddle point – the price of alternatives vs original meat – to parity.

That means that even as Beyond Meat sells more produce, its revenue per product declines. There’s also the need to get more Beyond Meat product into mainstream supermarkets and diversify away from foodservice partners. This is presumably a higher margin business space.

Lastly there’s growing competition in its space, especially from Impossible Foods which is rumoured to be looking at an IPO in the not too distant future.

Impossible has also been consistently lowering the price of its plant-based patties – most recently by 20 per cent. According to Barrons “that means that the suggested retail price of an Impossible Burger would be $5.49 (£3.88) in thousands of grocery stores across the country, with similarly planned price cuts for other markets, from Canada to Hong Kong”.

That’s still double the price of a normal beefburger but the price pressure and intense competition is obvious. It’s also worth noting that Impossible has, arguably, made more progress in developing its supermarket business compared to Beyond Meat.

On the positive side, most of the big established food brand giants haven’t been making much headway against Beyond Meat and Impossible. Despite intensive marketing Kellogg’s and Cargill – both of which have alt protein lines – haven’t proved much of a competitive threat.

One last longer-term threat comes in the shape of cultured meat, which will look and taste very much like traditional meat products. Cultured products may in the medium term disrupt the existing plant-based product.

Despite all the excitement about plant based products, we need to add a salty dose of realism on valuations. Beyond Meat currently boasts a market cap of over $9 billion (£6.36bn) but is only producing sales in the hundreds of millions of dollars range.

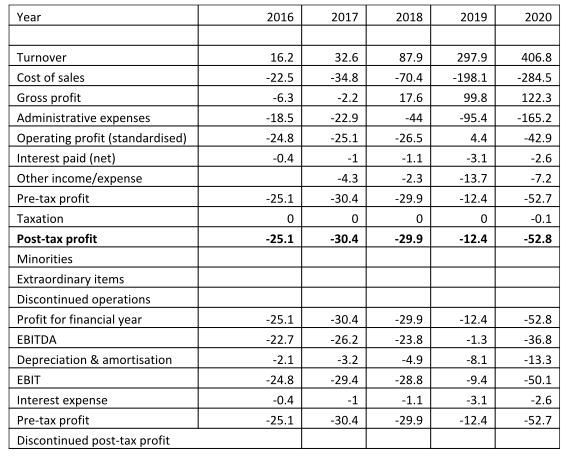

The chart below summaries the profit and loss account for the last few years. In 2020 sales totalled $406m (£287m) and the business produced a pre-tax loss (an increased one) of $52m (£36m).

To be fair to Beyond Meat, its core business is obviously in a disruptive growth phase (which was in turn disrupted by the pandemic) and it’s not fair (at this stage at least) to apply usual valuation metrics to the business, especially if it is likely to experience very substantial top line growth which should – at some point – mean it moves into profit.

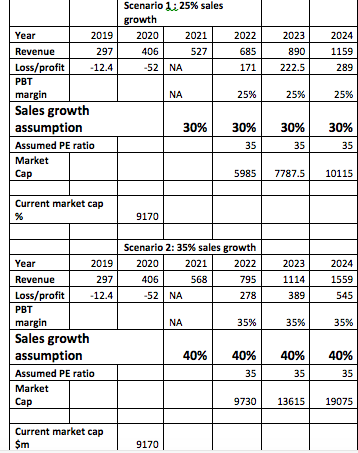

But even on this growth metric, we would argue that Beyond Meat is very highly priced in share price terms. The next table below is an attempt to pin a possible valuation for future growth. In the table we have assumed two scenarios: the first consistent top line growth of 30 per cent per annum for the next few years.

We have then assumed a pre tax profit margin of 25 per cent which we think is very generous.

Market leaders in consumer brands such as Unilever struggle to get pre tax margins much above the 15 to 25 per cent range. This gets us to possible sales in 2024 of just under $1 billion (£710m) and pre tax profits of just under $300m (£212m).

If we then generously assume a PE ratio of 35 in 2024, we get to a valuation of $10 billion (£7.1bn), just a shade over the current market cap.

In scenario two we forecast based on even more generous numbers. We assume consistent 40 per cent sales growth through to 20240 when sales hit $1.5 billion (£1.06bn) and we also assume a market beating 35 per cent profit margin – a demanding number we think given the intense competition. On this analysis Beyond Meat could be worth over $19 billion (£13.4bn) by 2024, well over twice the current market cap.

But this latter assumption assumes extra ordinary top line growth AND market leading profit margins. The point of this analysis is that for the current share price to make sense, we would need to make some pretty optimistic assumptions. And this is before we’ve even got to the near term risks and challenges. These are numerous and includes the fact that the business is losing chief financial officer Mark Nelson in May.

In addition, Beyond Meat is involved in various legal disputes : a California court recently ruled that Beyond Meat must pay supplier Don Lee Farms in their contract dispute. There’s also the real risk that Beyond Meat could experience modest inflation for some of its protein ingredients , which could also feed through into increased packaging and transportation costs. Lastly we’ve also made no assumptions about the need to keep capex spending high, or the possibility that price cuts eat into margins.

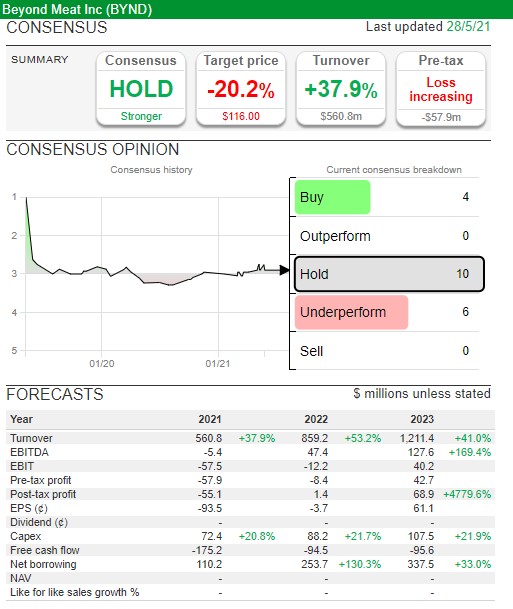

It’s fair to say that analysts have been growing more cautious on Beyond Meat in recent months, as the table below shows. Analysts’ expectations for profits and growth have been sliding for the last few months and the consensus price rating is now only a weak hold. The consensus seems to be that Beyond Meat will get to $1 billion (£710m) in sales by 2023 which we think is a tad ambitious.

As for individual analysts, Barrons has been publishing some of the more vocal opinions. We’ve summarised the key observations below:

2 August 2021

Paul Cuatrecasas

13 September 2021

Paul Cuatrecasas

30 June 2021

Paul Cuatrecasas

9 September 2021

David Stevenson